April 6, 2023

Things I Learned This Week While Eating a Pimento Cheese Sandwich

April 6, 2023

A Day Early. Happy Easter to all! My missive comes a day early because of the holiday.

Easter Sunday for me will be a dream come true. I will be at the Masters. Only took me decades and decades to make it but make it I shall, even though it will be 54 degrees and rainy. Wouldn’t you know it. I was picking shorts and wondering if it is too early for linen, and now I am back to rain gear and sweaters. I shall prevail!! And Kaari, after her recent 311-yard drive (wind helped!), she is excited to compare swings! Happy Holidays. (the Masters is famous for its $1.50 pimento cheese sandwich!)

OPEC+. A drop of 1.2 million barrels per day! Wow. On top of a 2 million barrels per day cut last October, bringing the total oil taken off the market at about 3.2% of total demand. That is a lot. Of course, many members were producing below quota levels anyway. So, really just 1.6% taken off the market, which presumably can be turned back on again somewhat quickly. Still a lot. That is not a surprise at all, to us or to the markets. Oil prices spiked but faded. The first tick of April 4th, the day of the announcement, oil traded at $80.81. Right now, oil is $80.65. OPEC+ must feel like Janet Yellen. Strong reassurance but not believed. The real cuts are half of announced, the productive capacity overall is brought into question. But we can’t have a run on OPEC.

Truth. Russia announced it has extended its 500,000-bpd cut which started in March. But so far there is no evidence that Russian production has dropped at all. It reminds me of the call of a U.S. recession. We have been saying it constantly, just around the corner, for over a year now. Russian oil production appears to have increased over the last month or so with the original “cut” aimed at the oil price cap designed by the Group of Seven.

Seasons Change. Years ago, we developed what we called our Timing Model. It looked at the monthly price of all OFS stocks relative to that year’s average price to isolate intra-year relative performance. We did this for the previous, at the time, 16 years of data for any OFS company that was public in any year for all twelve months. That aggregate variance was 16%, about four standard deviations in a sample that large. It basically said that stocks start to move up in late January, peak in early May and then bounce around for the rest of the year, with a slight move up at year end. We had seen several studies that the broad market forward discount’s highest correlation is about six months. We then noticed that the drivers of oil and gas activity, both commodity prices and activity, were almost exactly 180 degrees out of phase on an annual basis. Stocks moved up, even when activity was dropping, since the market was already discounting improved activity six months out. At the beginning of the year, there is little rush to spend budgets, and winter weather increases the cost of operations, usually by about 10%. Hunting season in the Rockies is still a thing as well. As a result, the rig count typically drops into the new year, until it bottoms in late spring and then moves up the rest of the year, eventually taking an early breather late in Q4 for holidays. 180 degrees out of phase. Oil and natural gas prices display the same price seasonality.

That Said… The U.S. rig count declines in Q1, by about 40 rigs and almost 5% of the total, as would be expected. Privates, who led activity last year, pulled the most rigs in Q1, with the public E&P companies and the majors actually increasing their rig counts slightly. If you remember from earlier writings, this switch has been well documented, with the driver moving from privates to publics. Eagle Ford took the biggest hit, down 23 rigs, followed by the Permian, down 9, the Anadarko down 7 and Appalachia down 5 rigs. This should not alarm anyone, as it was expected, based on historical seasonality that is very pronounced, and with now stronger oil and natural gas prices, we would not be surprised to see the rig count bottom over the next couple of months before starting to move up.

An Argument. I have been asked if Saudi Arabia cut production to get to their $95 target. With no offense, “target”? Yes, Saudi has more reserves than the U.S. but our production for the past few years has kept up, and briefly surpassed, Saudi Arabia’s oil production. I had to spell it out like that because for most of my career, the U.S. and Saudi tied in oil production and hitting 12mmbpd, is like me being tied with Tom Cruise for a leading role. But the idea that any country can or does have such a specific target. Years ago, we said $80 or $90 or $100 was their target. Other than in the very short term, no one can be that accurate. It is a very complex industry with a huge number of variables. It is easy to see that we are no longer the swing producer. It was fun and we kicked everyone’s butt, for a while. For two years, the U.S. grew crude oil production faster than any country ever has before. Think about that. We were the swing producer, the BMC, it felt great, but it cost us. From a recoverable oil perspective, we were a 69-year-old man who was still pretty good against a 19-year-old in shape. I can hold him, and sometimes get ahead. But I can’t win. The U.S. industry showed more innovation, technology, grit, determination. And we went ahead. But while we may not be leading anymore, we are a clear #2 and holding that position, right behind the leader, we still matter. And growth will come more from the adaptations of technology, in all areas of the company, its products and its people. No one can control or hit a discrete “target” of oil prices.

Whose Fault? OPEC+ announcing their oil cuts is a clear sign that OPEC and their largest producer Saudi Arabia are and always will be in charge of world oil prices no matter what anyone else thinks. Being “in charge” or the “swing producer” still doesn’t allow you to set oil prices but most definitely influence them. And guess who OPEC points the finger to on why they are cutting? The Biden administration's dumping of the SPR and not refilling it when prices got below $70 as President Biden said he would. This does not help Washington in terms of credibility of action in the global energy markets. Or sure seems to.

The Angle. The trajectory of today’s oil production recovery is a very different slope than the last few years. Remember what that steep slope cost the industry – billions and billions in losses. Makes the lower angle slope even prettier.

EIA Data.

U.S. crude production: indicated at 12,200 MBPD, flat from previous week, and up 400 MBPD from same period last year.

Refinery runs 15,615 MBPD, down 198 w/w and down 333 y/y. Utilization at 89.6%.

NEWS!?!? I don’t know if you’ve heard, but Donald Trump went to court this week. Oh. Wait. I just thought nothing else in the world happened this week because EVERY news outlet, opinion show, celebrity posts didn’t talk about ANYTHING else. So, on that note - I don’t want Mr. Trump to get the Republican nomination or have him run as an independent. But these are 34 versions of the same issue: 7 years ago, he told his lawyer to pay off a woman who was going to try and ruin his reputation or extort money. The way it was accounted for on Trump CO.’s books was obviously “mislabeled”, which is generally always treated as a misdemeanor, but the DA said it was done with intent of breaking another law, which makes it a felony. The other crime appears to be because he is Donald Trump. If anything, this is being engineered to increase Trump’s popularity to increase the chances he gets the nomination since the Democrats believe he is the only candidate they can beat.

Number Crunch. KeyBanc had produced several deep dive reports on well productivity in both the Midland and Delaware basins in late 2022, and recently updated their model, through mid-2022. “We come away incrementally bearish, given the pace and pervasiveness of well degradation across both sub-basins in the Permian Basin.”

Headlines.

Morgan Stanley CEO's pay rose 13% to $39.4 million in 2022.

Switzerland will cancel or cut bonuses for top Credit Suisse execs.

The 10-year yield fell for six straight days, the worst such streak since 2021.

Qatar and France’s Total partner on $10 billion natural gas project in Iraq.

Harbour Energy to cut 350 onshore North Sea jobs due to windfall tax.

Americans Are Actually Working Less These Days.

Biden downplays “surprise” OPEC oil production cut, says it won’t be as “bad as you think.”

One Opinion. The 42 U.S. E&Ps we track are tempering their 2023 capex increase to an average 17% in 2023 after an aggressive 54% boost in 2022. However, their budgets reflect significant shifts in capital among the major U.S. unconventional resource plays, based on commodity price trends and investment opportunities. – RBN Energy.

Smart Author. Bjorn Lomborg is the president of the Copenhagen Consensus and a visiting fellow at Stanford University’s Hoover Institution. His latest book is False Alarm: How Climate Change Panic Costs Us Trillions, Hurts the Poor, and Fails to Fix the Planet.

Snippets.

Saudi Arabia is constructing a new, $500 billion city in the desert that’s 33 times bigger than New York City and it’s building a Red Sea resort the size of Belgium.

Converting the world to entirely clean energy will require investment of $10 trillion over 20 years, but relying on fossil fuels will cost even more at $14 trillion, Tesla said in its Master Plan Part 3.

DMC Global said U.S. District Court found that its DS MicroSet setting tool did not infringe on the 035 patent against Repeat Precision and did not award any damages.

This year, analysts are pegging U.S. growth at 500,000 barrels a day. That’s substantial volume, but less than half the amount OPEC+ leaders cut at a single stroke last weekend, and certainly not enough to upset the cartel.

Credit. Up to $520 billion in debt needs to be written off to help developing nations at greatest risk of default return to sounder fiscal footing and meet climate and development goals, according to a Boston University report.

Deal. Noble Corporation priced a private offering of $600 million of new unsecured 8% senior notes due 2030.

It’s Not Just Trump. The Most Outstanding Player on the women’s NCAA winning team of LSU, Angel Reese says she, nor her team, would be visiting the White House. It seems that Jill Biden said she would invite the Iowa team as well, which did not sit well, but by the time she had walked it back, the damage was done. I don’t accept the apology because you said what you said … You can’t go back on certain things that you say … They can have that spotlight. We’ll go to the Obamas. “We’ll go see Michelle. We’ll see Barack.”

North America. The rig count has moved lower and is likely to decline a bit more with gas-directed rigs rolling off contracts. However, we do not expect pricing to adjust lower (sorry E&P’s) as the market remains exceptionally tight and any rig or frac provider that accepts a lower priced contract is a coward.

From My Friend James. The four pillars of modern civilization: 1) Ammonia (to make fertilizer); 2) Steel; 3) Cement; and 4) Plastics/ Petrochem combined consume ~17% of global energy supply while emitting ~20-25% of global CO2.

Don’t I Wish. Greg Abbott - “OPEC makes a surprise 1-million-barrel oil production cut. Texas might just counter that with a 1-million-barrel production INCREASE.”

Layoffs. We are trying to hire, and employee hiring and especially retention are some of our industry’s primary issues. So, to put the world in perspective – “After NPR's Major Layoff, Employees Accuse CEO Of Racism”. Really?? NPR??

Largest Layoffs of 2023, So far:

Amazon: 27,000 employees

Google: 12,000 employees

Meta: 10,000 employees

Microsoft: 10,000 employees

Goldman Sachs: 3,200 employees

Coinbase: 25% of employees

Zoom: 15% of employees

Glassdoor: 15% of employees

Twilio: 15% of employees

Indeed: 15% of employees

LendingClub: 14% of employees

Vimeo: 11% of employees

Docusign: 10% of employees

Salesforce: 10% of employees

Gemini: 10% of employees

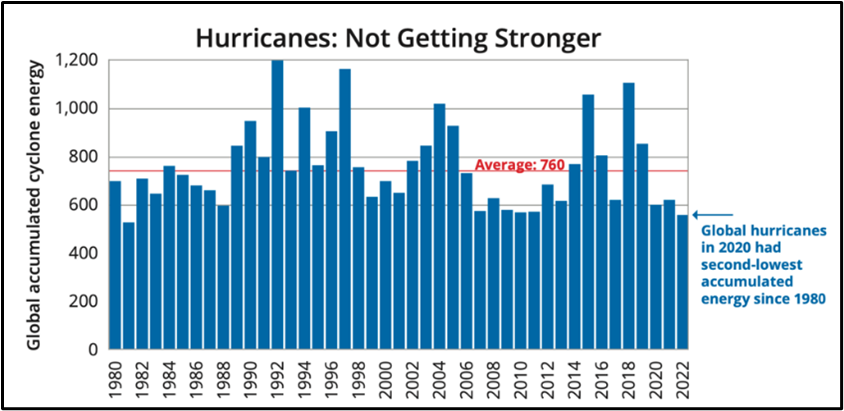

Some Will Disagree. Hurricanes are not getting more extreme. The chart shows global cyclones (hurricanes) over time. For the last several years, the dire warnings each year of the worst hurricane season in years never seemed to come about.

The Bears. And in case I have not upset some climate people enough, this chart caught my eye as well. Turns out, they aren’t on an extinction trend after all.

Credit Worries. Auto loan and credit card interest rates just hit a new record high.

Average Interest rates:

Credit Card: 24.5%

Used Cars: 14.0%

New Cars: 9.0%

Levels of Debt:

Total Household Debt: $16.5 trillion

Auto Loans: $1.6 trillion

Credit Card Debt: $986 billion

Student loans just hit a record $1.6 trillion.

A Rant. “Biden proposes to allow the offshore wind industry to kill up to 19% of the dolphins off the New Jersey coast. Taxpayers subsidizing pointless killing. So green. So humane. So ethical. So Orwellian. Where are the environmental groups? Where is PETA?”

Headlines #2.

Boston Children’s Hospital Director Calls for Drastic Increase in Capacity for Gender Surgery for Minors.

Exxon quits drilling in Brazil after failing to find oil. – WSJ

Asteroid the size of 33 armadillos to pass Earth Sunday. – NASA

Trans woman left sobbing in JFK airport after TSA agent hit her testicles.

Global Investment in the energy transition must increase by $47 trillion by 2050 to achieve 1.5C.

Quote. The OPEC cut was only possible because of the inability/unwillingness of the U.S. shale oil sector to grow at the same rate as it was in 2016-2020. With much less supply elasticity in the market today, OPEC is less worried about losing market share if it defends higher prices. - John Arnold. I certainly don’t disagree with the conclusion, but I have to quantify the “inability/unwillingness” statement. We are able to dramatically increase production. Not a question. We did it before and we are able to do it again. But we are unwilling to lose billions and billions of dollars like the last time we ramped up production in a big way. So that means the OPEC cut was inevitable. And other than increasing gasoline prices to levels still below most every other country, the U.S. oil and gas industry benefits from its own capital discipline and the benefits of that capital discipline, which then was further assisted by OPEC.

Nuke’m. I often get asked my opinion on the nuclear industry. I am a fan. The new modular reactors powered by thorium cannot go critical and are getting increased interest, and actual orders, from foreign countries. I lament the fact that it would take a few lifetimes to get them approved here. Maybe I was wrong. I hope so. A bipartisan group of U.S. senators introduced legislation aimed at reducing regulatory costs for licensing advanced nuclear reactor technologies, require the Nuclear Regulatory Commission to encourage licensing of nuclear facilities at brownfields and establish other routes to more quickly expand nuclear power. The Director of Nuclear Power Safety at the Union of Concerned Scientists, a nuclear watchdog group, dismissed the legislation as a “grab bag of special interest provisions.” As if renewables aren’t? And a cleaner, most longer lasting option? We can hope.

The Pendulum Swings. Berlin, Germany put a climate initiative on a special election ballot that would have bound the city to strive to be climate neutral by 2030, forcing local investment in renewable energy, building efficiency and public transport. All of those are important issues but for now, the Berliners voted against the measure by 92%-18%, easily constituting “a landslide”. The referendum was a test of whether the people of Berlin want to force a faster transition, knowing the goals can’t really be met, or work on improving the everyday lives of the people.

The Pitch. I am on the board of Merit Advisors, a tax valuation firm that has saved a great deal of money for many companies in our industry. I didn’t realize that SWD’s with no 3rd party use are exempt. I learn something from these guys all the time. They are having an event. Barrels and Clays is an exclusive "Invite Only" by Merit Advisors networking event for energy executives. Taking place on Tuesday, May 9th at the historic Stark Ranch in Gainesville, TX, this beautiful 6,000-acre ranch sits off the famous deep bend of the Red River where Texas meets Oklahoma. Attendees will have the unique opportunity to shoot clays over the picturesque Red River from Texas overlooking Oklahoma. The event promises an exciting afternoon of networking, drinks, food, and fun with various activities designed to engage attendees in a unique setting. In addition, the event will be supporting the Boys & Girls Club of Cooke County.

Event Highlights:

Competitive Clay Shoot

Clay Shoot Training

Whiskey Tasting

Networking BBQ Lunch

Stark Ranch Tour

Airboat Rides

Live Music

Barrels & Beyond (Mini-Conference)

If you are interested in an invitation, Register Here. https://cvent.me/qrGwrw

Any and all comments, arguments and rebuttals are welcome!

In addition to my association with PPHB, I serve on three private company boards. Merit Advisors is a property valuation company and I have long been a fan of optimizing how a business is run, not just the tools we make. Merit is in the business of savings companies’ money, actual cash, by doing a much more in-depth and realistic view of equipment and reserve valuations and I am very impressed with their work. I am also on the advisory board of Preng & Associates, a leading executive search boutique that specializes in all things related to Energy & Power. Nova is a gas compression company run by a very dynamic CEO with a very strong board and ownership.

I service on the Advisory board of the Energy Workforce & Technology Council (formerly PESA), the National Ocean Industries Association (NOIA), and the Maguire Energy Institute at SMU my alma mater.

jim

214-755-3914 | james.wicklund@pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 180 transactions exceeding $11 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.